Advanced Stock Pattern Prediction using LSTM with the Attention Mechanism in TensorFlow: A step by step Guide with Apple Inc. (AAPL) Data

Advanced Stock Pattern Prediction using LSTM with the Attention Mechanism in TensorFlow: A step by…

Introduction

drlee.io

Introduction

In the rapidly evolving world of financial markets, accurate predictions are akin to a holy grail. As we seek more sophisticated techniques to interpret market trends, machine learning emerges as a beacon of hope. Among various machine learning models, Long Short-Term Memory (LSTM) networks have gained significant attention. When combined with the attention mechanism, these models become even more powerful, especially in analyzing time-series data like stock prices. This article delves into the intriguing world of LSTM networks paired with attention mechanisms, focusing on predicting the pattern of the next four candles in the stock price of Apple Inc. (AAPL), utilizing data from Yahoo Finance (yfinance). All data is here.

Section 1: Understanding LSTM and Attention in Financial Modelling

The Basics of LSTM Networks

LSTM networks are a type of Recurrent Neural Network (RNN) specially designed to remember and process sequences of data over long periods. What sets LSTMs apart from traditional RNNs is their ability to preserve information for long durations, courtesy of their unique structure comprising three gates: the input, forget, and output gates. These gates collaboratively manage the flow of information, deciding what to retain and what to discard, thereby mitigating the issue of vanishing gradients — a common problem in standard RNNs.

In the context of financial markets, this capability to remember and utilize long-term dependencies is invaluable. Stock prices, for instance, aren’t just influenced by recent trends but also by patterns established over time. LSTM networks adeptly capture these temporal dependencies, making them ideal for financial time series analysis.

Attention Mechanism: Enhancing LSTM

The attention mechanism, initially popularized in the field of natural language processing, has found its way into various other domains, including finance. It operates on a simple yet profound concept: not all parts of the input sequence are equally important. By allowing the model to focus on specific parts of the input sequence while ignoring others, the attention mechanism enhances the model’s context understanding capabilities.

Incorporating attention into LSTM networks results in a more focused and context-aware model. When predicting stock prices, certain historical data points may be more relevant than others. The attention mechanism empowers the LSTM to weigh these points more heavily, leading to more accurate and nuanced predictions.

The Relevance in Financial Pattern Prediction

The amalgamation of LSTM with attention mechanisms creates a robust model for financial pattern prediction. The financial market is a complex adaptive system, influenced by a multitude of factors and exhibiting non-linear characteristics. Traditional models often fall short in capturing this complexity. However, LSTM networks, especially when combined with an attention mechanism, are adept at unraveling these patterns, offering a deeper understanding and more accurate forecasts of future stock movements.

As we proceed to build and implement an LSTM with an attention mechanism to predict the next four candles of AAPL’s stock, we delve into a sophisticated realm of financial analysis, one that holds the promise of revolutionizing how we interpret and respond to the ever-changing dynamics of the stock market.

Section 2: Setting Up Your Environment

To begin building our LSTM model with attention for predicting AAPL stock patterns, the first step is setting up our coding environment in Google Colab. Google Colab offers a cloud-based service that provides a free Jupyter notebook environment with GPU support, which is ideal for running deep learning models.

!pip install tensorflow -qqq

!pip install keras -qqq

!pip install yfinance -qqqSetting Up the Environment

Once installed, we can import these libraries into our Python environment. Run the following code:

import tensorflow as tf

import keras

import yfinance as yf

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

# Check TensorFlow version

print("TensorFlow Version: ", tf.__version__)This code not only imports the libraries but also checks the TensorFlow version to ensure everything is up to date.

Data Acquisition from yfinance

Fetching Historical Data

To analyze AAPL stock patterns, we need historical stock price data. Here’s where yfinance comes into play. This library is designed to fetch historical market data from Yahoo Finance.

Code for Data Download

Run the following code in your Colab notebook to download AAPL’s historical data:

# Fetch AAPL data

aapl_data = yf.download('AAPL', start='2020-01-01', end='2024-01-01')

# Display the first few rows of the dataframe

aapl_data.head()This script fetches the daily stock prices of Apple Inc. from January 1, 2020, to January 1, 2024. You can adjust the start and end dates according to your preference.

The Importance of Data Preprocessing and Feature Selection

Once the data is fetched, preprocessing and feature selection become crucial. Preprocessing involves cleaning the data and making it suitable for the model. This includes handling missing values, normalizing or scaling data, and potentially creating additional features, like moving averages or percentage changes, that could help the model learn more effectively.

Feature selection is about choosing the right set of features that contribute most to the prediction variable. For stock price prediction, features like opening price, closing price, high, low, and volume are commonly used. It’s important to select features that provide relevant information to prevent the model from learning from noise.

In the next sections, we will preprocess this data and build our LSTM model with an attention layer to start making predictions.

Section 3: Data Preprocessing and Preparation

Before building our LSTM model, the first crucial step is preparing our dataset. This section covers the essential stages of data preprocessing to make the AAPL stock data from yfinance ready for our LSTM model.

Data Cleaning

Stock market datasets often contain anomalies or missing values. It’s vital to handle these to prevent inaccuracies in predictions.

- Identifying Missing Values: Check for any missing data in the dataset. If there are any, you can choose to either fill them using a method like forward-fill or backward-fill or remove those rows entirely.

# Checking for missing values

aapl_data.isnull().sum()

# Filling missing values, if any

aapl_data.fillna(method='ffill', inplace=True)- Handling Anomalies: Sometimes, datasets contain erroneous values due to glitches in data collection. If you spot any anomalies (like extreme spikes in stock prices that are unrealistic), they should be corrected or removed.

Feature Selection

In stock market data, various features can be influential. Typically, ‘Open’, ‘High’, ‘Low’, ‘Close’, and ‘Volume’ are used.

- Deciding Features: For our model, we’ll use ‘Close’ prices, but you can experiment with additional features like ‘Open’, ‘High’, ‘Low’, and ‘Volume’.

Normalization

Normalization is a technique used to change the values of numeric columns in the dataset to a common scale, without distorting differences in the ranges of values.

- Applying Min-Max Scaling: This scales the dataset so that all the input features lie between 0 and 1.

from sklearn.preprocessing import MinMaxScaler

scaler = MinMaxScaler(feature_range=(0,1))

aapl_data_scaled = scaler.fit_transform(aapl_data['Close'].values.reshape(-1,1))Creating Sequences

LSTM models require input to be in a sequence format. We transform the data into sequences for the model to learn from.

- Defining Sequence Length: Choose a sequence length (like 60 days). This means, for every sample, the model will look at the last 60 days of data to make a prediction.

X = []

y = []

for i in range(60, len(aapl_data_scaled)):

X.append(aapl_data_scaled[i-60:i, 0])

y.append(aapl_data_scaled[i, 0])Train-Test Split

Split the data into training and testing sets to evaluate the model’s performance properly.

- Defining Split Ratio: Typically, 80% of data is used for training and 20% for testing.

train_size = int(len(X) * 0.8)

test_size = len(X) - train_size

X_train, X_test = X[:train_size], X[train_size:]

y_train, y_test = y[:train_size], y[train_size:]Reshaping Data for LSTM

Finally, we need to reshape our data into a 3D format [samples, time steps, features] required by LSTM layers.

- Reshaping the Data:

X_train, y_train = np.array(X_train), np.array(y_train)

X_train = np.reshape(X_train, (X_train.shape[0], X_train.shape[1], 1))In the next section, we will utilize this preprocessed data to build and train our LSTM model with an attention mechanism.

Section 4: Building the LSTM with Attention Model

In this section, we’ll dive into the construction of our LSTM model with an added attention mechanism, tailored for predicting AAPL stock patterns. This requires TensorFlow and Keras, which should already be set up in your Colab environment.

Creating LSTM Layers

Our LSTM model will consist of several layers, including LSTM layers for processing the time-series data. The basic structure is as follows:

from keras.models import Sequential

from keras.layers import LSTM, Dense, Dropout, AdditiveAttention, Permute, Reshape, Multiply

model = Sequential()

# Adding LSTM layers with return_sequences=True

model.add(LSTM(units=50, return_sequences=True, input_shape=(X_train.shape[1], 1)))

model.add(LSTM(units=50, return_sequences=True))In this model, units represent the number of neurons in each LSTM layer. return_sequences=True is crucial in the first layers to ensure the output includes sequences, which are essential for stacking LSTM layers. The final LSTM layer does not return sequences as we prepare the data for the attention layer.

Integrating the Attention Mechanism

The attention mechanism can be added to enhance the model’s ability to focus on relevant time steps:

# Adding self-attention mechanism

# The attention mechanism

attention = AdditiveAttention(name='attention_weight')

# Permute and reshape for compatibility

model.add(Permute((2, 1)))

model.add(Reshape((-1, X_train.shape[1])))

attention_result = attention([model.output, model.output])

multiply_layer = Multiply()([model.output, attention_result])

# Return to original shape

model.add(Permute((2, 1)))

model.add(Reshape((-1, 50)))

# Adding a Flatten layer before the final Dense layer

model.add(tf.keras.layers.Flatten())

# Final Dense layer

model.add(Dense(1))

# Compile the model

# model.compile(optimizer='adam', loss='mean_squared_error')

# Train the model

# history = model.fit(X_train, y_train, epochs=100, batch_size=25, validation_split=0.2)This custom layer computes a weighted sum of the input sequence, allowing the model to pay more attention to certain time steps.

Optimizing the Model

To enhance the model’s performance and reduce the risk of overfitting, we include Dropout and Batch Normalization.

from keras.layers import BatchNormalization

# Adding Dropout and Batch Normalization

model.add(Dropout(0.2))

model.add(BatchNormalization())Dropout helps in preventing overfitting by randomly setting a fraction of the input units to 0 at each update during training, and Batch Normalization stabilizes the learning process.

Model Compilation

Finally, we compile the model with an optimizer and loss function suited for our regression task.

model.compile(optimizer='adam', loss='mean_squared_error')adam optimizer is generally a good choice for recurrent neural networks, and mean squared error works well as a loss function for regression tasks like ours.

Model Summary

It’s beneficial to view the summary of the model to understand its structure and number of parameters.

model.summary()

Section 5: Training the Model

Now that our LSTM model with attention is built, it’s time to train it using our prepared training set. This process involves feeding the training data to the model and letting it learn to make predictions.

Training Code

Use the following code to train your model with X_train and y_train:

# Assuming X_train and y_train are already defined and preprocessed

history = model.fit(X_train, y_train, epochs=100, batch_size=25, validation_split=0.2)Here, we train the model for 100 epochs with a batch size of 25. The validation_split parameter reserves a portion of the training data for validation, allowing us to monitor the model's performance on unseen data during training.

Overfitting and How to Avoid It

Overfitting occurs when a model learns patterns specific to the training data, which do not generalize to new data. Here are ways to avoid overfitting:

- Validation Set: Using a validation set (as we did in the training code) helps in monitoring the model’s performance on unseen data.

- Early Stopping: This technique stops training when the model’s performance on the validation set starts to degrade. Implementing early stopping in Keras is straightforward:

from keras.callbacks import EarlyStopping

early_stopping = EarlyStopping(monitor='val_loss', patience=10)

history = model.fit(X_train, y_train, epochs=100, batch_size=25, validation_split=0.2, callbacks=[early_stopping])- Here, patience=10 means training will stop if the validation loss does not improve for 10 consecutive epochs.

- Regularization Techniques: Techniques like Dropout and Batch Normalization, which are already included in our model, also help in reducing overfitting.

Optional: These are more callbacks

from keras.callbacks import ModelCheckpoint, ReduceLROnPlateau, TensorBoard, CSVLogger

# Callback to save the model periodically

model_checkpoint = ModelCheckpoint('best_model.h5', save_best_only=True, monitor='val_loss')

# Callback to reduce learning rate when a metric has stopped improving

reduce_lr = ReduceLROnPlateau(monitor='val_loss', factor=0.1, patience=5)

# Callback for TensorBoard

tensorboard = TensorBoard(log_dir='./logs')

# Callback to log details to a CSV file

csv_logger = CSVLogger('training_log.csv')

# Combining all callbacks

callbacks_list = [early_stopping, model_checkpoint, reduce_lr, tensorboard, csv_logger]

# Fit the model with the callbacks

history = model.fit(X_train, y_train, epochs=100, batch_size=25, validation_split=0.2, callbacks=callbacks_list)Section 6: Evaluating Model Performance

After training the model, the next step is to evaluate its performance using the test set. This will give us an understanding of how well our model can generalize to new, unseen data.

Evaluating with the Test Set

To evaluate the model, we first need to prepare our test data (X_test) in the same way we did for the training data. Then, we can use the model's evaluate function:

# Convert X_test and y_test to Numpy arrays if they are not already

X_test = np.array(X_test)

y_test = np.array(y_test)

# Ensure X_test is reshaped similarly to how X_train was reshaped

# This depends on how you preprocessed the training data

X_test = np.reshape(X_test, (X_test.shape[0], X_test.shape[1], 1))

# Now evaluate the model on the test data

test_loss = model.evaluate(X_test, y_test)

print("Test Loss: ", test_loss)

Performance Metrics

In addition to the loss, other metrics can provide more insights into the model’s performance. For regression tasks like ours, common metrics include:

- Mean Absolute Error (MAE): This measures the average magnitude of the errors in a set of predictions, without considering their direction.

- Root Mean Square Error (RMSE): This is the square root of the average of squared differences between prediction and actual observation.

To calculate these metrics, we can make predictions using our model and compare them with the actual values:

from sklearn.metrics import mean_absolute_error, mean_squared_error

# Making predictions

y_pred = model.predict(X_test)

# Calculating MAE and RMSE

mae = mean_absolute_error(y_test, y_pred)

rmse = mean_squared_error(y_test, y_pred, squared=False)

print("Mean Absolute Error: ", mae)

print("Root Mean Square Error: ", rmse)

model:

- Mean Absolute Error (MAE): 0.0724 (approximately)

- Root Mean Square Error (RMSE): 0.0753 (approximately)

Both MAE and RMSE are measures of prediction accuracy for a regression model. Here’s what they indicate:

MAE measures the average magnitude of the errors in a set of predictions, without considering their direction. It’s the average over the test sample of the absolute differences between prediction and actual observation where all individual differences have equal weight. A MAE of 0.0724 means that, on average, the model’s predictions are about 0.0724 units away from the actual values.

RMSE is a quadratic scoring rule that also measures the average magnitude of the error. It’s the square root of the average of squared differences between prediction and actual observation. The RMSE gives a relatively high weight to large errors. This means the RMSE should be more useful when large errors are particularly undesirable. An RMSE of 0.0753 means that the model’s predictions are, on average, 0.0753 units away from the actual values when larger errors are penalized more.

These metrics will help you understand the accuracy of your model and where it needs improvement. By analyzing these metrics, you can make informed decisions about further tuning your model or changing your approach.

In the next section, we’ll discuss how to use the model for actual stock pattern predictions and the practical considerations in deploying this model for real-world applications.

Section 7: Predicting the Next 4 Candles

Having trained and evaluated our LSTM model with an attention mechanism, the final step is to utilize it for predicting the next 4 candles (days) of AAPL stock prices.

Making Predictions

To predict future stock prices, we need to provide the model with the most recent data points. Let’s assume we have the latest 60 days of data prepared in the same format as X_train: and we want to predict the price for the next day:

import yfinance as yf

import numpy as np

from sklearn.preprocessing import MinMaxScaler

# Fetching the latest 60 days of AAPL stock data

data = yf.download('AAPL', period='60d', interval='1d')

# Selecting the 'Close' price and converting to numpy array

closing_prices = data['Close'].values

# Scaling the data

scaler = MinMaxScaler(feature_range=(0,1))

scaled_data = scaler.fit_transform(closing_prices.reshape(-1,1))

# Since we need the last 60 days to predict the next day, we reshape the data accordingly

X_latest = np.array([scaled_data[-60:].reshape(60)])

# Reshaping the data for the model (adding batch dimension)

X_latest = np.reshape(X_latest, (X_latest.shape[0], X_latest.shape[1], 1))

# Making predictions for the next 4 candles

predicted_stock_price = model.predict(X_latest)

predicted_stock_price = scaler.inverse_transform(predicted_stock_price)

print("Predicted Stock Prices for the next 4 days: ", predicted_stock_price)

Let’s predict the price for the next 4 days:

import yfinance as yf

import numpy as np

from sklearn.preprocessing import MinMaxScaler

# Fetch the latest 60 days of AAPL stock data

data = yf.download('AAPL', period='60d', interval='1d')

# Select 'Close' price and scale it

closing_prices = data['Close'].values.reshape(-1, 1)

scaler = MinMaxScaler(feature_range=(0, 1))

scaled_data = scaler.fit_transform(closing_prices)

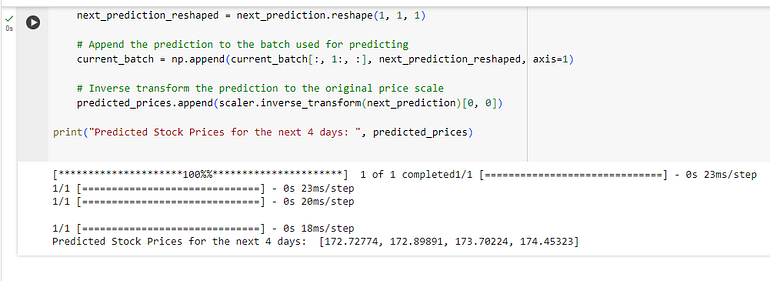

# Predict the next 4 days iteratively

predicted_prices = []

current_batch = scaled_data[-60:].reshape(1, 60, 1) # Most recent 60 days

for i in range(4): # Predicting 4 days

# Get the prediction (next day)

next_prediction = model.predict(current_batch)

# Reshape the prediction to fit the batch dimension

next_prediction_reshaped = next_prediction.reshape(1, 1, 1)

# Append the prediction to the batch used for predicting

current_batch = np.append(current_batch[:, 1:, :], next_prediction_reshaped, axis=1)

# Inverse transform the prediction to the original price scale

predicted_prices.append(scaler.inverse_transform(next_prediction)[0, 0])

print("Predicted Stock Prices for the next 4 days: ", predicted_prices)

Visualization of Predictions

Comparing the predicted values with actual stock prices visually can be very insightful. Below is the code to plot the predicted stock prices against the actual data:

!pip install mplfinance -qqq

import pandas as pd

import mplfinance as mpf

import matplotlib.dates as mpl_dates

import matplotlib.pyplot as plt

# Assuming 'data' is your DataFrame with the fetched AAPL stock data

# Make sure it contains Open, High, Low, Close, and Volume columns

# Creating a list of dates for the predictions

last_date = data.index[-1]

next_day = last_date + pd.Timedelta(days=1)

prediction_dates = pd.date_range(start=next_day, periods=4)

# Assuming 'predicted_prices' is your list of predicted prices for the next 4 days

predictions_df = pd.DataFrame(index=prediction_dates, data=predicted_prices, columns=['Close'])

# Plotting the actual data with mplfinance

mpf.plot(data, type='candle', style='charles', volume=True)

# Overlaying the predicted data

plt.figure(figsize=(10,6))

plt.plot(predictions_df.index, predictions_df['Close'], linestyle='dashed', marker='o', color='red')

plt.title("AAPL Stock Price with Predicted Next 4 Days")

plt.show()

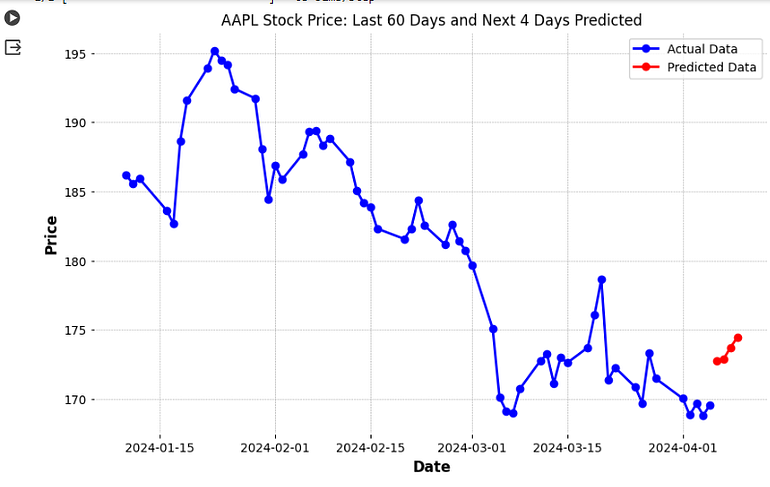

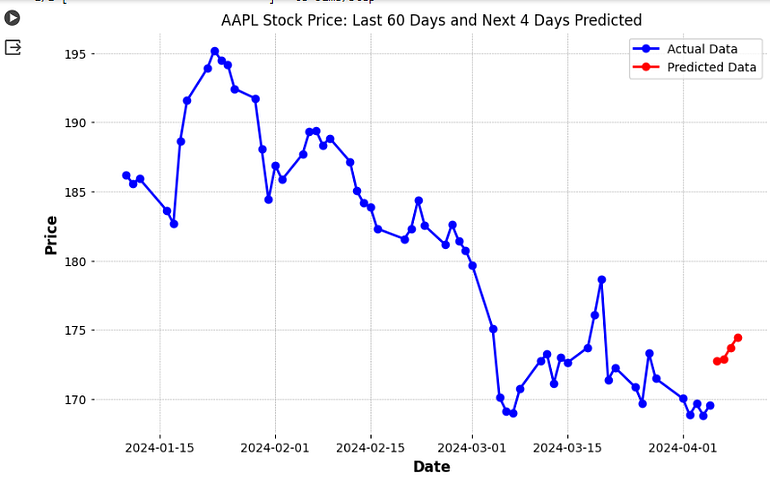

Final Visual for Predictions:

import pandas as pd

import mplfinance as mpf

import matplotlib.dates as mpl_dates

import matplotlib.pyplot as plt

# Fetch the latest 60 days of AAPL stock data

data = yf.download('AAPL', period='64d', interval='1d') # Fetch 64 days to display last 60 days in the chart

# Select 'Close' price and scale it

closing_prices = data['Close'].values.reshape(-1, 1)

scaler = MinMaxScaler(feature_range=(0, 1))

scaled_data = scaler.fit_transform(closing_prices)

# Predict the next 4 days iteratively

predicted_prices = []

current_batch = scaled_data[-60:].reshape(1, 60, 1) # Most recent 60 days

for i in range(4): # Predicting 4 days

next_prediction = model.predict(current_batch)

next_prediction_reshaped = next_prediction.reshape(1, 1, 1)

current_batch = np.append(current_batch[:, 1:, :], next_prediction_reshaped, axis=1)

predicted_prices.append(scaler.inverse_transform(next_prediction)[0, 0])

# Creating a list of dates for the predictions

last_date = data.index[-1]

next_day = last_date + pd.Timedelta(days=1)

prediction_dates = pd.date_range(start=next_day, periods=4)

# Adding predictions to the DataFrame

predicted_data = pd.DataFrame(index=prediction_dates, data=predicted_prices, columns=['Close'])

# Combining both actual and predicted data

combined_data = pd.concat([data['Close'], predicted_data['Close']])

combined_data = combined_data[-64:] # Last 60 days of actual data + 4 days of predictions

# Plotting the actual data

plt.figure(figsize=(10,6))

plt.plot(data.index[-60:], data['Close'][-60:], linestyle='-', marker='o', color='blue', label='Actual Data')

# Plotting the predicted data

plt.plot(prediction_dates, predicted_prices, linestyle='-', marker='o', color='red', label='Predicted Data')

plt.title("AAPL Stock Price: Last 60 Days and Next 4 Days Predicted")

plt.xlabel('Date')

plt.ylabel('Price')

plt.legend()

plt.show()

Conclusion

In this guide, we explored the complex yet fascinating task of using LSTM networks with an attention mechanism for stock price prediction, specifically for Apple Inc. (AAPL). Key points include:

- LSTM’s ability to capture long-term dependencies in time-series data.

- The added advantage of the attention mechanism in focusing on relevant data points.

- The detailed process of building, training, and evaluating the LSTM model.

While LSTM models with attention are powerful, they have limitations:

- The assumption that historical patterns will repeat in similar ways can be problematic, especially in volatile markets.

- External factors like market news and global events, not captured in historical price data, can significantly influence stock prices.

References

- TensorFlow Documentation: https://www.tensorflow.org/

- Keras API Reference: https://keras.io/api/

- Yahoo Finance (yfinance) for Stock Data: https://pypi.org/project/yfinance/

- Pandas Documentation: https://pandas.pydata.org/

- Matplotlib for Visualization: https://matplotlib.org/

This guide should serve as a starting point for those interested in applying deep learning techniques in financial markets. Continuous exploration and experimentation are encouraged to refine and adapt these methods for more sophisticated applications.

Addendum: Compute from any date:

import yfinance as yf

import numpy as np

import pandas as pd

from sklearn.preprocessing import MinMaxScaler

from datetime import datetime, timedelta

def predict_stock_price(input_date):

# Check if the input date is a valid date format

try:

input_date = pd.to_datetime(input_date)

except ValueError:

print("Invalid Date Format. Please enter date in YYYY-MM-DD format.")

return

# Fetch data from yfinance

end_date = input_date

start_date = input_date - timedelta(days=90) # Fetch more days to ensure we have 60 trading days

data = yf.download('AAPL', start=start_date, end=end_date)

if len(data) < 60:

print("Not enough historical data to make a prediction. Try an earlier date.")

return

# Prepare the data

closing_prices = data['Close'].values[-60:] # Last 60 days

scaler = MinMaxScaler(feature_range=(0, 1))

scaled_data = scaler.fit_transform(closing_prices.reshape(-1, 1))

# Make predictions

predicted_prices = []

current_batch = scaled_data.reshape(1, 60, 1)

for i in range(4): # Predicting 4 days

next_prediction = model.predict(current_batch)

next_prediction_reshaped = next_prediction.reshape(1, 1, 1)

current_batch = np.append(current_batch[:, 1:, :], next_prediction_reshaped, axis=1)

predicted_prices.append(scaler.inverse_transform(next_prediction)[0, 0])

# Output the predictions

for i, price in enumerate(predicted_prices, 1):

print(f"Day {i} prediction: {price}")

# Example use

user_input = input("Enter a date (YYYY-MM-DD) to predict AAPL stock for the next 4 days: ")

predict_stock_price(user_input)'Python' 카테고리의 다른 글

| Raspberry Pi NTP Server (0) | 2024.04.16 |

|---|---|

| Pickle In Python (0) | 2024.04.15 |

| hexa string to Floating-point value (0) | 2024.04.02 |

| [python]reactpy (0) | 2024.03.19 |

| mqtt 참고사이트 (0) | 2024.03.19 |

댓글